Sharing the cake, giving employees Equity

28 April 2026

This article focuses on the EMI scheme (Enterprise Management Incentives) is a UK government-backed tax-advantaged employee share option scheme designed for small, growing companies to attract and retain key employees. Employees are granted the option to buy shares at a fixed price, and any increase in share value between the grant and exercise of the option is generally exempt from Income Tax and only subject to a favourable Capital Gains Tax (CGT) rate of 10%

Other employee share schemes are used (CSOP, SAYE, SIP) but EMI is by far the most common.

Employer Considerations

Setting Up an EMI Share Option Scheme: Key Steps and Considerations

1. Confirm Eligibility and Define Objectives

Ensure both your company and your target employees meet EMI criteria. Criteria below:

- Your company must have gross assets of £120 million or less,

- fewer than 500 full-time employees, be independent,

- and carry on a qualifying trade.

Individual employees must work at least 25 hours per week (or 75% of their time) for you, and hold no more than 30% of the company’s shares.

2. Obtain a HMRC Valuation

You need a formal valuation from HMRC to set the minimum exercise price. Submit your valuation application and allow 2–4 weeks for approval. Once you receive the agreement on the market value, lock in both the “agreed market value” and any unaffected market value metrics, as these underpin tax relief and cap your liability exposure.

Employee options must be granted within 90 days of valuation (but you can get an extension from the EMI team if needed)

3. Design Scheme Rules and Documentation

Craft the core plan documents:

- EMI Scheme Rules: Define eligibility, exercise price, vesting schedule (time-based or performance-based), exercise window, and exit triggers.

- Option Agreements: Tailored for each participant, referencing your master rules.

- Leaver Provisions: Decide treatment on resignation, redundancy, or bad leaver events.

- Anti-Dilution and Transfer Restrictions: Protect existing shareholders and maintain alignment.

This documentation phase sets expectations for participants and ensures compliance from day one.

4. Secure Board and Shareholder Approvals

Hold a board meeting (or written board resolution) to adopt the EMI rules and create the option pool. If required by your articles, obtain shareholder consent via ordinary resolution. Document all minutes and signed resolutions these form part of your statutory records and back your HMRC filings.

5. Register the Scheme with HMRC

Log into HMRC’s Employment Related Securities (ERS) service and register your EMI Scheme. You’ll receive a reference number online within 7 days. Registration must precede any option grant to preserve tax advantages.

6. Grant Options to Employees

Allocate options from your pool using the agreed exercise price. Issue and sign individual option agreements, then prepare option certificates. Ensure each grant references the HMRC valuation date and scheme reference. Communicate clearly with option-holders about vesting conditions and exercise mechanics.

7. Submit a Joint NIC Election

Before any exercise, file a joint election with HMRC to benefit from reduced National Insurance Contributions. You only need one approved election per employer; thereafter you can issue blank election forms to new participants without fresh HMRC sign-off.

HMRC Reporting and Ongoing Compliance

EMI Notification Deadlines

For grants on or after 6 April 2024, you must notify by 6 July following the tax year end. Late notifications risk forfeiting income tax and NIC reliefs for both you and your employees.

Annual ERS Return

Each tax year (up to 5 April), file an ERS return by 6 July detailing any EMI grants or other employment-related securities movements. Even if you’ve made no grants, you must submit a nil return until the plan is formally closed on HMRC’s system. Penalties apply for late or incorrect filings.

Using Templates and Administrators

If reporting for more than 30 participants, use HMRC’s Excel templates; for 30 or fewer, you can file directly via the ERS online service. Appoint at least two ERS administrators under your Government Gateway account to ensure continuity especially important if one administrator is unavailable unexpectedly.

Employee Considerations

What is a share option?

A share option gives its holder the right, but not the obligation, to buy a company's shares at a predetermined price, known as the exercise price or strike price, within a specified period.

Strike / Exercise price - this is what it costs you to buy each share. Usually really low in early stage startups.

Tax Implications for Employees

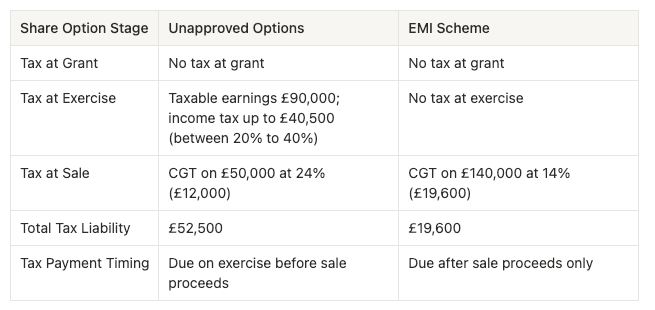

Unapproved options vs EMI schemes

With an EMI scheme, tax is only incurred on the value of shares when they're awarded rather than when they’re exercised. This is the biggest difference between EMI schemes and other schemes.

- Capital Gains Tax is applied at a lower rate of 14% instead of 24%.

- Shares cannot be sold within 24 months of the option grant for this discount to apply.

For £10,000 worth of shares at grant, with £100,000 value at exercise, and £150,000 value when sold. Tax implications.

Vesting Schedules, Cliffs, Leaver Status

Vesting Schedule - The vesting schedule sets out a period of time over which you’re given the share options. This is usually 4 years. For example, if you were granted 1000 shares in a 4 year vesting schedule you would be granted an average of 250 shares per year. If you leave before 4 years you won’t get all the options. You may also be subject to a bad leave clause (more on that in a bit).

Cliff - usually 1 year. Options don’t vest in the 1st year.

Bad leaver - dismissed due to gross misconduct will no longer have access to any of their vested options.

Good leaver – has the right to purchase any vested options for a set period of time after leaving the company. This window typically lasts 90 days.

Are share options actually worth it?

It really depends on the success of the company that you’re in. According to Carta between 10 to 20% of seed startups will make it to Series B (the point at which you might consider it viable for buyout). Low single digits will be acquired 1-2%.

Say you get 0.5% of a company at Seed, where the company was valued at £1 million. Value of shares is £50,000. The prospective exit could be £50 million to £100 million in 5 years, but only 1% chance of happening.

Expected Profit from Exit = £75million * 0.25% (due to dilution) * 1% = £1875

Expected value from an exit is actually very low at an early stage so it is not worth financially sacrificing a large amount of salary on a strictly financial basis.

Key Reading

https://carta.com/uk/en/learn/equity/share-options/